By Edward Hugh

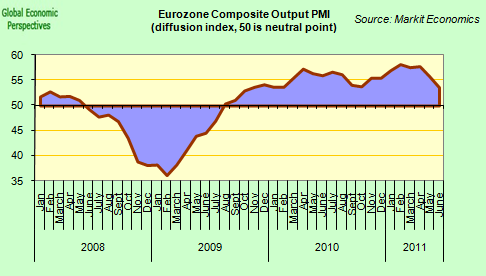

The June Flash PMI reports, which were out on Thursday, do not make for agreeable reading, in the sense that while the French and German economies both continued to expand during the month, their rate of expansion, and in particular in the leading manufacturing sector, seems to have dropped sharply, and for the second month running. In contrast, the economies on the Eurozone periphery moved closer to outright contraction. All in all the survey results only add to concerns about the global recovery which came into focus after the May PMI results (see my To QE3 or Not to QE3).

{kind=link}

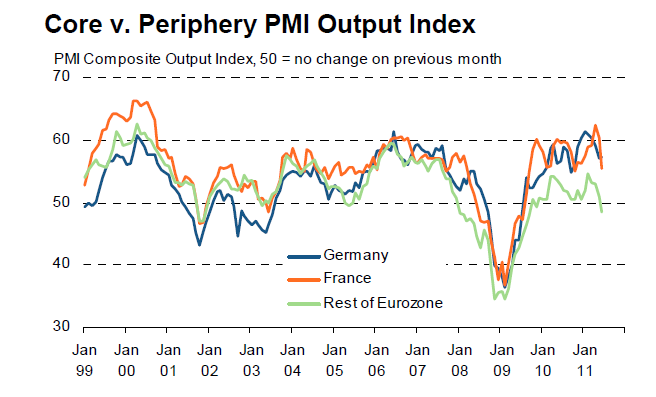

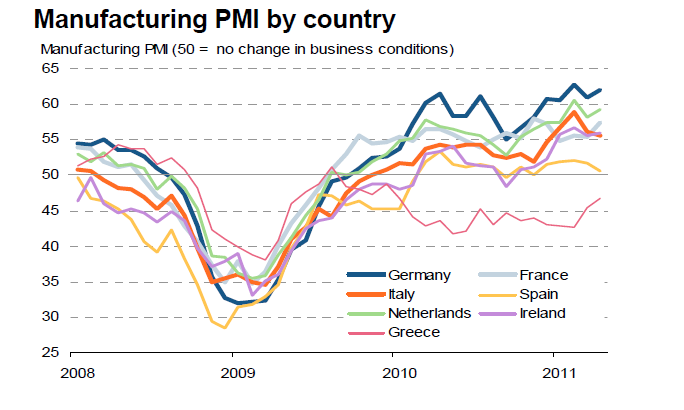

At this point detailed information is only available for the French and German economies, but there is little doubt that the pace of the slowdown in the core will mean that the peripheral economies are about to experience a double dip (and particularly worrying in this sense is the way Italian growth has been drifting downwards) and may well fall back into recession (in those cases where they have not already done so). Outside of France and Germany, manufacturing output (the PMIs are composite diffusion indexes, and the headline reading measures the aggregate of various components of which output levels are only one) fell for the first time since November 2009, with the rate of decline being the fastest since September 2009. So this is nothing to be sneezed at! As can be seen from the chart below, in all cases indicator readings are falling, but in the periphery case they are falling into recession territory.

{kind=link}

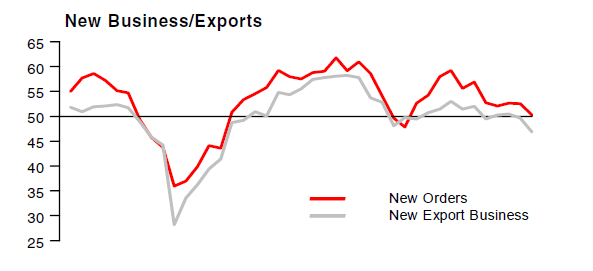

Most importantly, we should note that it is the manufacturing sector which is falling most sharply, and in an export driven recovery this has to be THE leading indicator for Europe’s economies. In addition export order growth is now at its lowest level in the nine months.

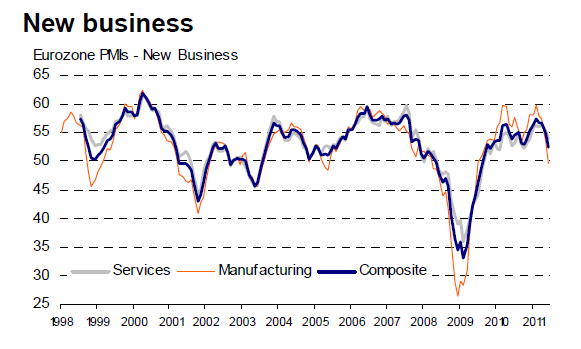

New business rose at the weakest rate since November 2009, led by the first (albeit small) decline in manufacturing new orders since July 2009 (see chart below). New export orders for manufactured goods rose only modestly, posting the smallest increase since September 2009.

{kind=link}

This impression of slowing global demand for exports was also confirmed by the Chinese manufacturing PMI flash reading which showed that Chinese export orders actually declined during the month (China is the only country beyond the Eurozone to do a flash PMI, and Chinese manufacturing as a whole barely expanded). These manufacturing export indicators are important, as they constitute what could be called long leading indicators (and here’s ECRI’s Managing Director Lakshman Achuthan explaining on Fox TV what long leading indicators are, why this slowdown isn’t simply about Japan supply chains, or the weather, and why what we are facing – barring recourse to QE3 – looks like something more than a “global soft patch”).

{kind=link}

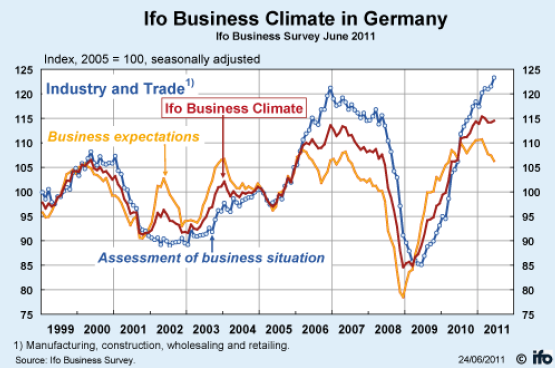

Another “long leader” came in with a strange reading in June, and that was the German IFO. On the face of it, the gung-ho analysts thought the reading was a good one, but that interpretation could be rather simplistic. Let’s look closely at the chart:

{kind=link}

What we should be looking at here isn’t the composite (red) line, but the sub components, and the one to get your head round is the business expectations component (yellow line). This peaked in February, after moving sideways from November 2010, and there is no sign of it turning up again. This is the sort of thing Lakshman Achuthan talks about in his interview. If we want to argue that what is happening is just a “soft patch” then we need to see indicators like the expectations component of the IFO to start turning upwards again, and at present there is no sign of that, so at present we lack grounds for asserting the “soft patch” argument, and in this context the fact that conditions in June were better than expected is neither here nor there, since that only tells us June was a batter month than expected, but virtually nothing about the future.

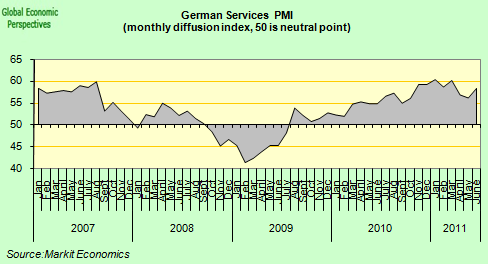

If we look at the German services PMI we can get some clues as to why the IFO overall business climate reading came in above expectations (up at 114.5 from 114.2 in May, while consensus expected a fall to 113.4): the expansion in services activity accelerated during the month, following a loss of momentum in the two previous months.

{kind=link}

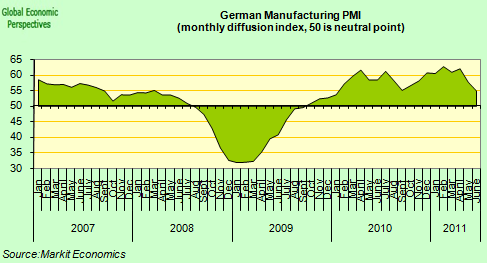

In contrast manufacturing activity fell sharply.

{kind=link}

As the Markit report says:

“Sector-specific data nonetheless highlighted a marked divergence between manufacturing and services in June. While services business activity increased at a robust and accelerated pace, the latest rise in manufacturing output was the slowest since September 2010. Consequently, an improved performance from the service sector boosted the overall figures for the German private sector in June. The moderation in manufacturing production growth coincided with another sharp slowdown in new order gains. June data pointed to the weakest expansion of new business in the sector since July 2009. Manufacturers also indicated the least marked rise in new export orders since the current period of growth began in October 2009″.

Yep, the slowest rise in new export orders since July 2009. Now there’s another long leading indicator for you, and it is showing red. If German export orders don’t grow then finally the German economy doesn’t grow, since Germany is an export driven economy, whatever those who live in eternal hope of a recovery in German domestic consumption may tell you.

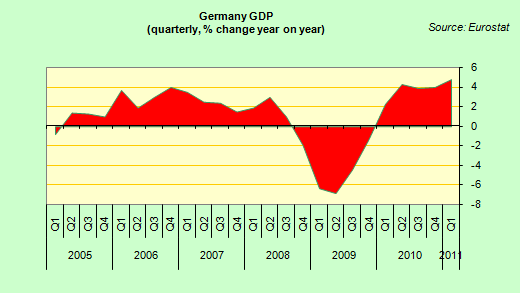

Now if we go back to the IFO chart for a moment, note that the assessment of the current business situation hasn’t peaked yet, although it must surely be close to doing so. The last time this component in the indicator peaked was at the end of 2006, and guess what else coincided with that peak? The cyclical wave of the last German GDP expansion (in terms of year-on-year growth) peaked at (more or less) exactly the same time.

{kind=link}

Now obviously Germany didn’t go on to enter recession for over a year (5 quarters to be exact), which means we probably aren’t talking about a recessionary slowdown in Germany at this point, but what we may be talking about is a German economy which is passing its cyclical high point (shudders go out along the periphery on reading this, since the peripheral economies haven’t even gotten their recoveries seriously started yet), and if this is the case there will be clear implications for Eurozone momentum.

As I say, we have no flash PMI’s for the periphery, but if we look at the May reading, it is clear that while Greece is in a world of contraction all of its its own, Italy and Spain have been steadily weakening, and it is quite possible they both countries will register contraction this month (Ireland has somehow escaped the trend up to this point).

{kind=link}

As Chris Williamson, Chief Economist at Markit said in the comment accompanying the report:

“The euro area’s economic growth surge has lost momentum at a worrying rate in the past two months. While the average PMI reading for the second quarter as a whole suggests that the economy grew by around 0.6%, down from 0.8% in the first quarter, the reading for June was consistent with a quarterly growth run rate of just 0.4%. Manufacturing growth has slowed especially sharply, slipping close to stagnation in June. Even German manufacturing, the driving force of the region’s recovery, has seen a marked deterioration in output and new orders growth – linked to a large extent to a severe weakening of export order book growth. Meanwhile, the euro area excluding France and Germany has fallen back into contraction for the first time since late-2009″.

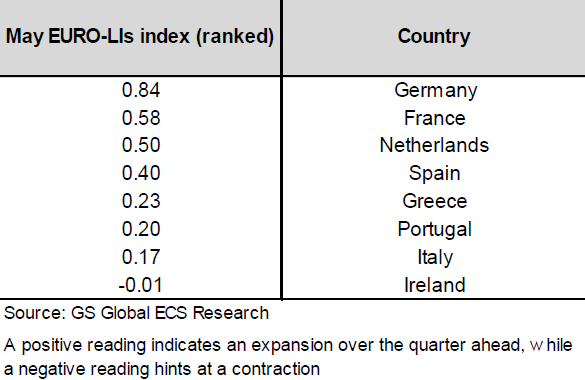

Curiously, just this week Goldman Sachs European Department have published (European Weekly Analyst June 16) a new set of leading (not long leading) indexes (attempting to identify trends for the three months ahead), and their findings broadly corroborate the PMI outlook. What is especially noteworthy in their list is the very weak showing from Italy (see my Is Italy Not Spain The Real Elephant In The Euro Room? for background).

{kind=link}

As they say in their report:

Italy and Spain languish. As expressed in our latest views published on Italy (see EWA 11/18) and Spain (see our European Views “Spain: Mitigating concerns about regional deficits, but mixed views on short-term growth prospects”, June 6, 2011), Italy and Spain may lack momentum in the quarters ahead, as suggested by the quasi-flat EURO-LIs in May.

To Raise Or Not To Raise In July?

Which brings us to the ECB, and the potential policy implications of these results. The first thing to note is that the flash PMIs suggested that inflation continued to ease back in June, particularly in the leading manufacturing sector. As the accompanying report states, “the easing in output price inflation in manufacturing was driven by a further steep easing in input price inflation from the survey-record rate of increase seen in February. A ten-month low in the rate of manufacturing input price inflation was accompanied by a five-month low in the service sector. Measured across both sectors, input costs rose at the slowest rate since October, down sharply from March’s peak”. I don’t know if that is clear enough for decision makers over at the ECB yet, but supply side inflation is definitely on the wane at this point, and since economic activity is also weakening this environment is hardly supportive of a rate rise decision.

{kind=link}

Really, the issue is not whether or not the ECB would be right to go ahead with a further rate rise in this situation – personally I think it is pretty obvious they wouldn’t as I made plain from the start in my Chronicle of a Policy Error Foretold post on the CNBC blog before this charade even got started. The issue is whether the Governing Council of the ECB will prove themselves flexible enough to change discourse in the face not just of Greek default woes, but of slowing inflation and growing recessionary risks?

In other words, are ECB decision makers moved more by developments in the real economy, or by an obsession with trying to “normalise” interest rates as quickly as possible using the happy circumstance of temporarily above target inflation as the excuse (however much M. Trichet denies they have this kind of agenda)? In fact he even has the justification that – as he said himself on Friday – that the risk signals for financial stability in the euro area are “flashing red”. Surely, at this critical moment in the history of the common currency he has stewardship over, he would not want to go down in history as the Montagu Norman of the Great Global Recession. But then, maybe I am being unfair. Possibly it is another ghost that is keeping Monsieur Trichet thrashing around on his pillow at night: the one formed by the precedent of the Bank of Japan in 2007, who when they found themselves forced to call a rapid halt to a previously much paraded rate hike programme after only one measly 0.25% rise. History, as they say, does repeat itself, even the ECB’s own recent history, but let us hope that this time we will not have to face an example of “once bitten, twice shy”.

Also see my Roubini Global EconoMonitor Blog “Don’t Shoot The Messenger“.