By Edward Hugh

Evidence which would enable us to assess the full economic impact of the Japanese earthquake and tsunami is still hard to come by. There is a lot of talk of supply chain disruptions, but little in the way of detailed evidence to back up assertions of the more anecdotal kind. Even the latest set of manufacturing PMI data has decidedly left the jury out on the topic.

{kind=link}

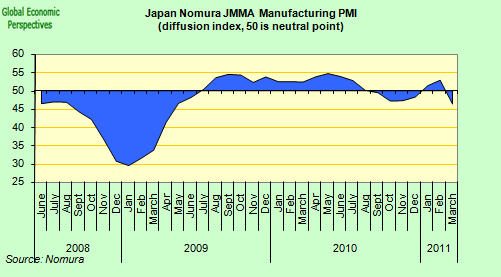

Evidently in Japan there was a clear and substantial drop in activity, but that was only to be expected . The Japanese March PMI slumped to a two-year low of 46.4, down from February’s reading of 52.9, the largest one month drop on record.

{kind=link}

Commenting on the Japanese Manufacturing PMI survey data, Alex Hamilton, economist at Markit and author of the report said:

“March PMI data provide the first indication of how output at small, medium and large sized Japanese manufacturers was affected by the events following the Tohoku earthquake on 11 March. The PMI slumped to a two-year low, suffering the largest monthly fall in points terms since the survey began in 2001, exceeding the drops seen after 9/11 and the collapse of Lehmans. The latest index reading is consistent with a decline in Japanese industrial production of around 7.0% on a 3m/3m basis”.

“Suppliers’ delivery times lengthened at a survey record pace amid widespread disruption in the supply chain resulting from the disaster. These delays could affect production in coming months and drive input price inflation even higher than the two-and-a-half year peak seen in March.”

At the same time it is hard to disagree with this conclusion, presented by Nomura economist Richard Koo in a recent report on the subject:

Any analysis of Japan’s position vis-à-vis the rest of the world needs to start with the question of whether Japan was running a trade surplus or deficit. A trade deficit implies the world has lost a customer: ie, demand: whereas a surplus would mean the world has lost a producer, namely, a supplier of products and intermediate goods. Inasmuch as Japan boasts the world’s third-largest trade surplus after China and Germany, I think the world has lost an important supplier.

Supplier countries’ products are typically in demand for one of two reasons: either they are cheap or they are essential. A key to distinguishing between the two is the exchange rate. When a nation’s currency is cheap relative to those of its trading partners, its exports tend to fall into the first (“cheap”) category, whereas exports from countries with a fully or over-valued currency tend to fall into the second (“essential”) group.

The Japanese yen has been the strongest currency in the developed world since the Lehman-inspired financial shock. Its strength was reaffirmed when it surged into the Y76-77 range against the US dollar in the wake of the earthquake. Japan has continued to run one of the world’s largest trade surpluses in spite of an extremely strong currency. Inasmuch as this is evidence that there are many businesses around the world that must buy Japanese products regardless of the cost, I suspect that many of Japan’s exports cannot be easily substituted.

But elsewhere, at least on the surface, there was little sign that companies were being held back by any substantial shortage of components.

Digging a little deeper, while manufacturing output strength weakened slightly from February, survey respondents still indicated companies were raising output rapidly. On the other hand it is hard to sort the wood from the trees here, since global output could weaken for any of a number of reasons, most of them nothing whatsoever to do with Japan.

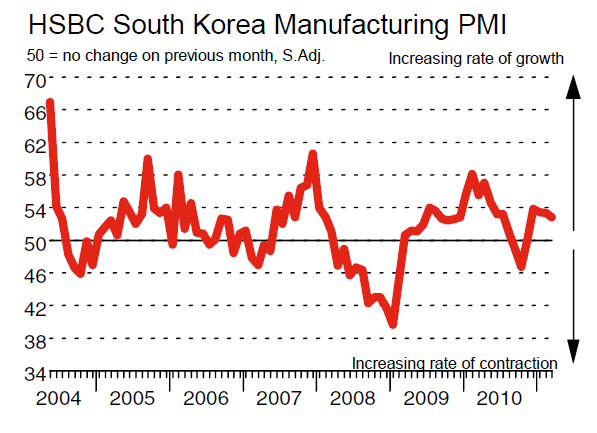

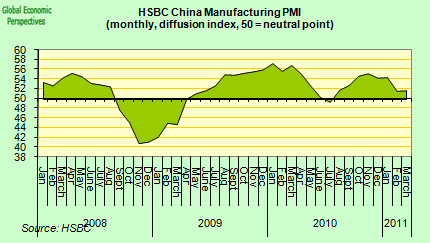

More significantly, manufacturing activity did slow in South Korea, and failed to really recover in China following the end of the new year holiday season. These two countries are among the most closely integrated with the Japanese economy.

{kind=link}

{kind=link}

Commenting on the China Manufacturing PMI survey, Hongbin Qu, Chief Economist, China & Co-Head of Asian Economic Research at HSBC said:

“The Final March manufacturing PMI confirmed that the pace of manufacturing expansion has stabilised after slowing in February. This implies economic growth is only moderating rather than slowing too much. More importantly, price hikes also started to slow in March. All these confirm our view that quantitative tightening is working. So as long as Beijing keeps tightening for another three to four months, inflation should start to slow meaningfully in 2H2011.”

On the other hand, there has been plenty of earlier evidence that the Chinese economy may now be slowing somewhat, and this for its own domestic reasons. So it is hard to know what is attributable to a Japan impact here, and what isn’t.

Certainly it does seem that economies in Asia are now slowing somewhat, and since the region has been one of the main drivers of the global economy, then this slowing will be noticed in those economies which are most dependent on exports.

Curiously, both in Europe and in China the final PMI reading was below the initial flash estimate, which could suggest that problems mounted a bit as the month advanced, with those responses which came in later being slightly less optimistic.

Either way, the big issue isn’t the supply chain disruption one – since lost output can (in general) be quickly recovered in this context, especially given the degree of surplus capacity which still exists in the global manufacturing system – rather the question is one of where exactly we are in the current global cycle?

Many Emerging market economies have plenty of scope for continuing rapid expansion, as long as the markets are still willing to fund them. And risk sentiment doesn’t seem to be an issue at the moment, although forthcoming monetary policy decisions at central banks in both the developed and the developing world make the mid term outlook rather more uncertain than it was six months ago.

{kind=link}

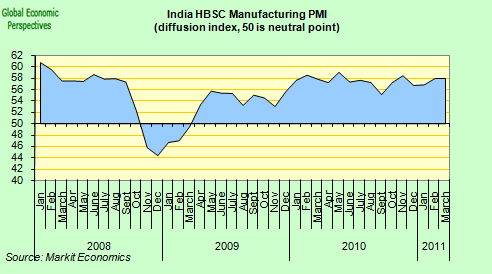

Commenting on the India Manufacturing PMI survey, Leif Eskesen, Chief Economist for India & ASEAN at HSBC said:

“The momentum in India’s manufacturing sector held up well in March, suggesting that growth is not an immediate concern. Output growth kept up the pace and the inflow of new orders accelerated, holding promise of a continued strong momentum in output in the months ahead. However, capacity constraints are tight as reflected in the increase in the backlog of works. Also, manufacturer’s are facing ever steeper increases in input costs due to tight labour markets and rising material costs, which are increasingly being passed on to output prices. In turn, this calls for further tightening of monetary policy to tame inflation pressures.”

{kind=link}

{kind=link}

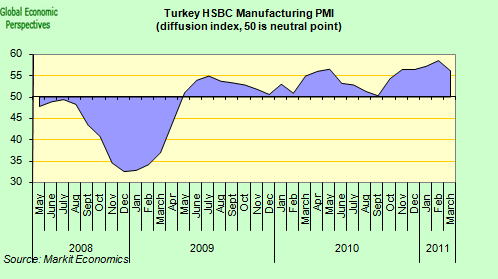

Commenting on the Turkey Manufacturing PMI survey, Dr. Murat Ulgen, Chief Economist for Turkey at HSBC said:

“Turkish manufacturing sector performance eased somewhat in March from its record high level in the previous month, though it still remained comfortably stronger than past averages. The slight slowdown in the rate of expansion was caused by output and new orders, both of which also expanded at slightly lower, but still markedly strong rates. There was a solid slowdown in new export order growth, possibly reflective of uncertainties in the Middle East & North Africa region, while backlogs of work fell despite the weaker expansion of output. Employment conditions continued to improve as manufacturers continued to hire more workers to meet robust demand and production. There was a slight decline in stock of purchases in March due to shortages of raw materials, as reported by survey participants, that was also evident in the continued lengthening of supplier delivery times. While both input and output prices rose at slower rates than in February, they both continued to signal pipeline inflationary pressures in the manufacturing industry.”

{kind=link}

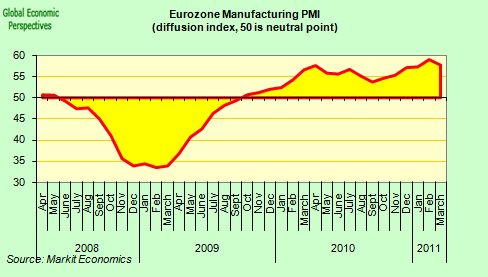

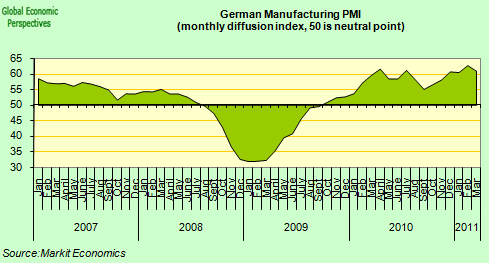

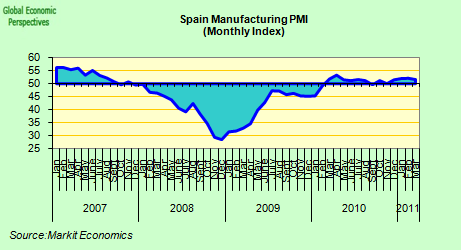

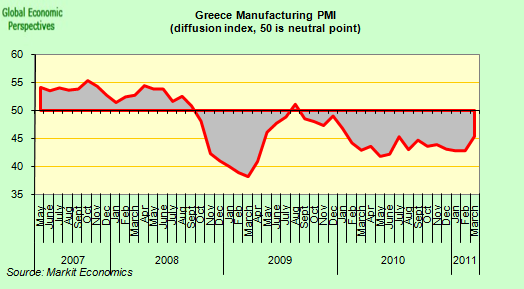

In the Eurozone,where the headline PMI slipped from 59 in February to 57.5, the results followed a now familiar pattern, with Germany, France and Italy all showing quite robust expansions, while Greece, Spain and Ireland continue to struggle, even if in each case the performance was an improvement on earlier months. Of the three, only Greece continued to show a contraction in activity, even if this was at a slower rate than previously.

{kind=link}

Chris Williamson, Chief Economist at Markit said:

“The Eurozone’s manufacturers continued to report buoyant business conditions in March. Despite the slight easing since February, the data are consistent with industrial production growing at a quarterly rate of 2%, spearheading the region’s recovery.“National divergences are marked, however, with surging output growth driving record job creation in Germany, while weak or falling production led to ongoing job losses in Spain and Greece.

“The record jump in average prices charged for goods will further encourage the European Central Bank to increase interest rates sooner, rather than later, which may drive further divergences among member states as higher borrowing costs hit already weak demand in the periphery.”

{kind=link}

Commenting on the final Markit/BME Germany Manufacturing PMI survey data, Tim Moore, senior economist at Markit and author of the report said:

“German manufacturing growth cooled during March, but the latest figures confirm an exceptionally strong performance for the sector across Q1 2011 as a whole. Firms continued to benefit from steep gains in inflows of new business during March, helped by the fastest expansion of export orders for ten months.

“The survey’s fifteen-year anniversary was marked by a series record rise in manufacturing employment levels, as firms continued to step up production capacity in response to steep improvements in order books.

“March data indicated higher levels of purchasing and stocks of inputs, reflecting concerns about lengthening supplier delivery times as well as greater production requirements. Strong global demand for raw materials was cited as the primary reason for supply chain delays, and only a small proportion of the survey panel cited the earthquake in Japan.

“Surging raw material and transportation costs meanwhile meant that factory gate price inflation accelerated to a level last seen in the wake of the January 2007 VAT rise.”

{kind=link}

Commenting on the Spanish Manufacturing PMI survey data, Andrew Harker, economist at Markit and author of the report, said:

“The latest PMI survey indicated a continuing divergence between demand in domestic and foreign markets, with the latter proving the main source of new order growth. Meanwhile, a record rise in output prices was recorded, although the rate of charge inflation remains much weaker than that seen for input costs as firms struggle to fully pass on price rises to clients.

{kind=link}

Phil Smith, Economist at Markit and author of the Greece Manufacturing PMI said:

“Waning domestic and international demand for Greek manufactured goods continued to hurt the sector during March. Crucially, firms were left with little choice but to absorb sharp input price inflation and find savings elsewhere. To some extent, this came in the form of rapid stock depletion. Hope, however, might be taken from the fact that business wins by surveyed firms fell at the slowest rate for ten months.”

But the issue this raises is that the global economy must now be getting somewhere near the peak of this cycle, at least in terms of manufacturing activity. Central banks across the globe are moving into tightening mode, and much of the low lying fruit has now been eaten, so the issue for the fragile economies on Europe’s periphery (who are now totally dependent on movements in demand elsewhere for growth) is how they will fare, not during the highpoint, but as and when the current expansion slows.

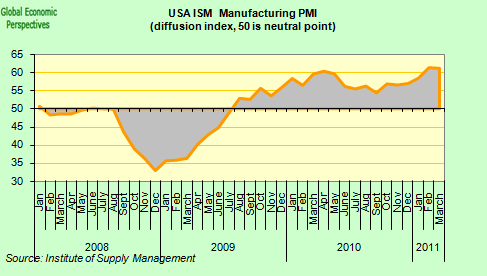

In the US, the PMI index, compiled by the Institute for Supply Management, edged down from 61.4 in February to 61.2 in March, but stood at a level close to a 27-year high.

{kind=link}

Norbert Ore, chairman of the ISM, said “the component indexes of the PMI remain at very positive levels and signal strong sector performance in the first quarter”. Despite the positive result this month, doubts remain about where exactly we are in the cycle at this point. Danske Bank’s Signe Roed-Frederiksen thinks we may be near the peak, which doesn’t mean a collapse in activity, but simply that from this point the rate of expansion may slow:

US ISM manufacturing declined from 61.4 to 61.2 in March. This was marginally higher than consensus expectations of 61.0 and our estimate of 60.7. However, details of the export suggest that the ISM will continue lower over the coming months.

New orders dropped to 63.3 from 68.0 and although inventories declined as well, the drop was more modest. This means that the two order-inventory differentials declined further and continue to signal a downward correction in the ISM index. The ‘new orders customer inventory’ differential, which has proven the most reliable on short-term movements, suggests the ISM should decline to around 57. The ‘new orders-inventory’ differential suggests a more pronounced slowdown to 56.

New export orders weakened to 56.0 from 62.5 possibly reflecting the slowdown in Asian growth while supplier deliveries increased to 63.1 from 59.4, indicating a slower pace of deliveries. Prices paid rose further to 85.0 from 82.0 reflecting the increase in commodity prices and upward pressure on input prices.

That said, even a moderate decline from the current level would still leave the ISM index at a healthy level.

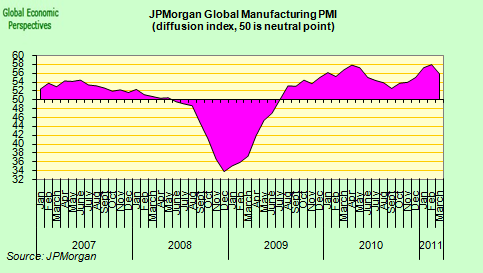

Globally, the headline PMI reading was 55.8, well above the historical average and the level of 50 that attempts to separate expansion from contraction, But down from the 57.4 registered in February, largely as a result of the slump in activity in Japan.

As David Hensley, economist with JPMorgan, put it: “There was little visible sign of supply-chain disruptions in the March surveys, but this effect is likely to be more visible in Asian emerging markets in April.”

The main concern expressed by the authors in their monthly report referred to the inflationary threat coming from a rapid rise in the prices of inputs and evidence that manufacturers were passing these on. Certainly, in this sense, the report will do little to deter decision makers at the ECB from raising interest rates when they meet on Thursday.