The following is a guest post by Polyvios Petropoulos, a former university professor of economics and management in the US.

Petropoulos contends that the austerity package drawn up by the IMF is not credible and that everyone knows Greece cannot meet its commitments. He ends the post with a four-step scenario he deems actually plausible.

Petropoulos’ view differs considerably from the usual fare at Credit Writedowns. However, his is a good alternate view of the Greek situation from a Greek perspective. Pay particular note to his assertions about government salaries and the credibility of government finances in Greece and elsewhere.

Zeus (Δίας), the Greek god, gave Europe the name of his beloved woman (Ευρώπη), hoping that she would be immortal. The question now is: Will the European dream end where it began, in Greece, or will it end in catharsis, as all Greek tragedies do?

It is only in the last few months that most commentators realized that this crisis is not about Greece only, that it is a European and, eventually, a global sovereign debt crisis, and that Greece is not even the worst case. Anyone who still thinks that this is only a Greek (or a GIPS) crisis should take a look at this table, published three months ago, which shows that Greece is only 16th in external debt as % of GDP among developed countries, whereas Germany is 14th, with a slightly higher figure, believe it or not, France is 8th, and the UK is 3rd . As to structural deficit-to-GDP, it is higher in the US (7.8%) and the UK (7.6%) than it is in Greece (6.1%). See here.

Have the Greeks been “fiddling” with their statistics? Maybe they did. But we should also realize that no budget figures of any country can be dependable, credible, or comparable, and furthermore figures are easy to play with, as there are no standard, uniform, accounting rules for country budgets, and no surveillance whatsoever. Let me elaborate: Do the figures of any country include off-budget items, unfunded and contingent liabilities, future or deferred commitments, government guarantees, bank-insurance schemes, the debt/liabilities of public corporations, pension schemes and health systems? What about leasing and lease-backs? Are “top secret” expenditures for defence and intelligence activities included and shown in government budgets? Are expenditures presented when contracts are signed or when they will be paid for? Are revenues brought forward by factoring etc.?

What about swaps, securitisation and other gimmicks used to fiddle with the figures? Let’s look at the allegation that Greece used cross currency swaps to reduce its debt, and whether it is the only country that has used them. First of all, “swaps” and other “instruments of mass destruction” were not invented in Greece or promoted by Greeks. Secondly, the GS swap deal was not done before but after Greece had joined the EMU (in 2002). Thirdly, such swaps were at the time acceptable by the EU commission and the Eurostat, as the EU commission spokesman Amadeu Altafa declared in Brussels on Feb. 15th. Which other countries have used or were involved in swaps? Too many to even list them here, let alone to describe the boring details of the exact deals of each: Italy, Spain, Portugal, France, Belgium, UK, and Germany (yes), among others. Even Mr. Bernanke, in his testimony before the Committee on Financial Services on Feb. 10th, says that the Fed “entered into temporary currency swap agreements” and has used “reverse repos”.

A lot has been written about corruption in Greece. And surely there is corruption in Greece, as there is everywhere. I tried the Google search engine a few days ago, and typed “corruption in…(country)”. I got 28,600,000 links for the US, 8,930,000 for France, 8,490,000 for the UK, 6,910,000 for Germany, 4,720,000 for Italy and 2,680,000 for Greece. You may say that this is not necessary indicative and dependable about the amount of corruption in the different countries, but neither are the rankings of “Transparency International”. According to an opinion survey conducted in Nov. 2009 by the Eurobarometer, 78% of Europeans say that “corruption is a major problem in the EU”. A “fakelaki” in Greece is a sort of a tip in most cases. Like the “tip” you may give to the traffic policeman in some countries…(you know which one I mean) to avoid getting a traffic ticket (don’t ever try it in Greece by the way). Now, other more serious types of corruption, such as bribing, are also prevalent in Greece, primarily in tax revenue depts. Many foreign companies (particularly German) bribe Greek officials to get contracts. And I‘ll remind my German friends that it takes two to tango. A lot has been written about other types of corruption in major countries of the western world, such as campaign contributions, sponsoring, lobbying and regulatory agencies staffed by ex-managers of the organizations they are supposed to regulate. Does it remind you of anything?

Who is to blame? “Everyone is a sinner”, according to J. Stark, the ECB chief economist. I have also elaborated who some of the sinners are in this article. But the main sinners of course are the successive Greek governments. It is true that fiscal discipline has been lax. Steps to reduce the budget deficit should have been taken in the “good times”, i.e. in the years before the beginning of the Great Recession. Then, when the recession hit the country in 2007-8, stimulus measures were needed to prop up the economy, but they were not taken, perhaps because the country could not afford them. And now, in 2010, fiscal stabilization has to be carried out. Unfortunately, populist politicians did not realize what was happening or what they should be doing all these years, and they didn’t understand what the correct timing of each phase of economic policy should have been, and they did nothing to increase competitiveness, which is at the root of the problems. It was an unnecessary extravagance for Greece to organize the Olympic Games in 2004, at a cost that exceeded 10 b. euros. And Greece has a defense budget which is roughly one third of its deficit, primarily due to Turkish provocations in the Aegean Sea. One word to the supporters of speculators and naked CDSs: Nobody is saying that they have created the crisis, as most of them are trying to disprove. What sensible people are saying is that they are exacerbating the crisis.

Have the Greeks been living beyond their means? Here is the answer:

{kind=link}

Average salaries in Greece are about 73% of the average eurozone salary. According to Eurostat and GSEE data, 60% of Greek pensioners receive less than 600 euros per mo. And 85% receive below 1050 euros per mo. Greek pensions are about 55% of the average eurozone pension, despite inaccurate claims about pensions made in the international media. The usual age for retirement of most people in Greece has been 65 yrs, except for some very special cases in the public sector, which are now being revised upwards –and rightly so- with a new pensions law.

Do Greek households spend more than they earn by borrowing a lot? No. In fact, German households owe more than Greeks. See here. Are Greeks not as hard-working as Germans, or others, as some are saying? Here are the facts. As you can see, Greeks are the most hard-working people in the OECD countries (with the exception of Koreans). The average Greek worker works 2120 hours per year – 690 more than a German worker. (Source: OECD).

Now let me turn to the IMF/EU package concluded with Greece recently. In a press conference published on the IMF website on May 9th, you may read (all bolds are mine):

“Today, the IMF has demonstrated its commitment to doing what it can to help Greece and its people,” Strauss-Kahn said. “The road ahead will be difficult, but the government has designed a credible program that is economically well-balanced, socially well-balanced—with protection for the most vulnerable groups—and achievable. Implementation is now the key.”

Let me consider these claims one by one and be absolutely clear and precise: First of all, the IMF/EU program (particularly the EU portion) is no “help” or “aid” or “rescue”, or even “bailout”, as the IMF, the EU and various commentators are saying. It consists of a series of loans, in fact non-concessional loans, as it is clearly stated in the Q&A session of the IMF here, with unprecedented draconian conditionality and the normal interest rate which is charged by the IMF in all cases. As to the EU portion, it is given at an even higher interest rate, which should be turned down by the Greek government. Paying 5-6% interest rate, when the country’s GDP growth is -4% p.a., clearly makes the country’s debt problem unsustainable, as has been shown by several economists. In judging interest rates, it should also be remembered that these loans are senior to all other Greek debt.

Second, it was not offered to help the “Greek people”. It was offered to help the bondholders, the bankers, the euro, and to avoid contagion with its nasty consequences for the EU and the global economy, as it is clearly stated elsewhere in the Q&A session mentioned above.

Third, there is absolutely no “protection for the most vulnerable”, as one would have expected from the “socialist” (or “ex-socialist”?) head of the IMF, or the “socialist” Greek government for that matter, and this claim is made several times in both of the documents mentioned above. The opposite is true. A mere listing of some of the austerity measures will suffice to prove my assertion:

-A meager so-called “social solidarity allowance” for destitute people was abolished, despite assurances in the IMF Q&A session that “the targeting of social expenditures will be revised to strengthen the social safety net for the most vulnerable”.

-Despite assurances in the Q&A session that “minimum pensions and family support instruments will not be cut”,all public and private–sector pensions and allowances have been cut, all the way down to meager pensions of 450, 500, 550 euros per month etc., which are well below the poverty line (making it impossible for old pensioners to survive), and this is what the majority of pensioners receive. This must be reversed for both human and economic reasons. On the other hand, nothing has been changed regarding the 300 Greek MPs, who receive a substantial pension after only 8 yrs in parliament!

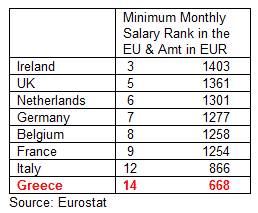

-Reduction of the salaries of even the lowest-paid civil servants. The 13th and 14th bonuses, which are often mentioned as a sign of extravagance, should have been incorporated in the 12 monthly salaries, and Greek salaries would still be lower then the EU average. (See comparison of total Greek and EU salaries above.)

-Freezing of the lowest salaries and pensions for the next few years, although inflation is already galloping above 4% p.a., well above the EU average, and may go even higher, despite the IMF claim at the press conference that“inflation is expected to remain below the euro average.”

-VAT (value added tax), which was much higher in Greece than in Portugal and Spain, was raised by about 20% on all goods, including basic foodstuffs, which make up the majority of poor people’s purchases.

-Sales taxes were raised on –supposedly- luxury goods…such as gasoline (+50%), cigarettes, beer, wine etc. I say to the poor people of Greece: For heaven’s sake, don’t drive, and stay away from all these sinful products!

To be fair, according to an interview of Mr. Papaconstantinou, the Greek finance minister, a few days ago, the reduction of the pitiful pensions of the private sector was not imposed by the IMF officials in Athens, but by the EU officials. My guess is that it must have been decided at the insistence of an official appointed to the negotiating team by “Frau Nein”, who wants blood, sweat and tears imposed on the Greek people.

The agreement reached between the IMF, the EU and the Greek government says nothing about reducing the number of MPs and ministries, or the number of civil servants, says nothing about capital gains, about selling part of the real estate owned by the state and the church, and is vague about taxing the rich, reducing drastically the state’s expenses, making politicians accountable for corruption with strict laws, about privatizations, competitiveness and export-led growth. Greeks should be allowed to bring their deposits (over 200bn) back from abroad without the 5% penalty. Housing construction, which is the economy’s “steam engine”, was further penalized. Labor market reforms should have been more daring. For obvious reasons, nothing has been announced by the Greek government about the sensitive subject of military expenditures, although the IMF says that they will be reduced. I assume that Greeks will require proportional reductions from Turkey before actually implementing such reductions. Also Greece’s EU partners, from whom Greece buys most of the weapons, will not be thrilled about this. Nothing was said also about the great oil reserves waiting to be drawn from the Aegean Sea, worth several trillions. Implementation of the measures announced is also questionable. It’s indicative that dates by which income tax returns for 2009 must be submitted were again postponed recently until as late as May-June of this year. In the meantime the tax people are looking for swimming pools in the backyards of the Greeks, as if this were a sign of great wealth…

Regarding competitiveness, which is indeed of paramount importance, the IMF makes simplistic observations, as is the case with many other commentators. First of all, competitiveness is not only a question of unit labor costs, but depends on many other factors as well. Secondly, looking only at the comparative percentage increase of unit labor costs in Greece since 1999, as most do, is not enough, because absolute figures of wages and salaries, which are much lower compared to the EU average, as I have shown above, do matter as well, and are not mentioned in any of the IMF documents, or by the media. ULCs in absolute figures are lower in Greece than in any of the other GIIPS countries, as well as in the UK and Denmark. (See here.) Finally, nothing is said about the intra-EU imbalances, or about the divergences in competitiveness, trade balances and inflation, which were created in favor of the core EU countries of the north vis-à-vis the southern peripherals since 1999, as a result of the common market and pegged currency, as economic theory postulates that they are bound to.

Will the “program” work? The claim made in the IMF documents is that the “program” (including the inhuman austerity conditions and targets) is “achievable”, “feasible” and “sustainable”. On this point, however, the IMF of course has not been able to convince some of the most prominent economists and commentators (Krugman, Feldstein, Stiglitz, Rogoff, Eichengreen, Johnson, Roubini, Rodnik, Buiter, Reinhart, Fitoussi, Wyplosz, Wolf, Munchau, among others, mentioned here in no particular order.) All are saying in one way or another that the numbers do not add up. In other words, the arithmetic shows that even with this IMF/EU package, the Greek debt is not sustainable. (See in particular Buiter’s latest 65-page research report “Sovereign Debt Problems in Advanced Industrial Countries”.)

Nor did the IMF convince the markets with this package. In fact, I am beginning to believe that nothing will convince them. Even though there was initially some improvement, not because of the IMF/EU package for Greece, but after the latest eurozone stabilization program of nearly one trillion, the latest ECB decision to in effect monetize the debt by buying government bonds (as all other central banks have been doing all along), the USD loan swaps, the laxity by the ECB with respect to accepting government bonds of a lower rating as collateral, and the plans to establish an EU rating agency, which were all announced very recently. Other factors which may, or may not, impress the markets are the imminent eurozone decisions regarding economic coordination and governance (see the EU commission proposals here), and the impressive -40% reduction of the Greek deficit in the first quarter of this year.

Despite the theories of some ivory-tower economists, about the supposed “rationality”, “discipline” and “efficiency” of the markets, markets and speculators are not at all rational. Greece is not alone in the debt trap, not even the worst case, to be penalized by the markets so harshly. Recent EU figures show that total debt is 224pc of GDP in Greece, 272pc in Spain and 331pc in Portugal. Also the gross external debt of Greece is 168.2pc of GDP, Portugal’s is 232.7pc and Spain’s is the same as Greece’s (Ireland’s is a record 979.4pc). But the spreads on 10-yr debt were recently 7.75pc for Greece (after dropping from previous incredible heights), and only 3.92pc for Spain and 4.62pc for Portugal. Does this make any sense? And yet I do not wish to be overly suspicious or conspiratorial…

On “restructuring” or “rescheduling” of Greek debt, the IMF is adamant in both documents: No way. Again many of the economists previously mentioned are not at all convinced. The discussion which is now going on is whether to restructure with or without a haircut, or to do a “voluntary” rescheduling, as I have suggested as Option C here, and whether this should be done sooner or later, with or without IMF’s and eurozone’s consent, without a euro exit or with euro exit and drachma devaluation. Discussions of the Greek government with Lazard, the investment bank who are specialists in debt restructuring, make some people suspicious.

A plausible scenario could be as follows in this sequence of steps: (1) Start receiving IMF/EU funds in tranches, preferably after revising terms and EU interest rate, as I have suggested, and start selling bonds to ECB directly, or through Greek banks. (2) Evaluate progress of implementation and results every month, revising measures where needed. (3) If all goes according to plan, continue implementing. If not, reschedule debt with IMF/EU consent. (4) If no consent given, or, if still no progress is made, then exit eurozone and devalue the drachma.