In Europe, there has been a lot of talk about Germany’s second largest bank, Dresdner Bank, which is looking to get sold by its parent Allianz. Allianz, which also owns U.S. bond giant PIMCO, has had only trouble with Dresdner since it bought the company at the top of the market in 2000. In a scenario that reminds me of Daimler-Benz and Chrysler, Allianz now wants out.

The situation has been complicated, because interest has been diluted by the rival sale of Postbank by Deutsche Post, the former state-owned postal service. Nevertheless, there have been a number of suitors looking at Dresdner. The two most interesting are Commerzbank and China.

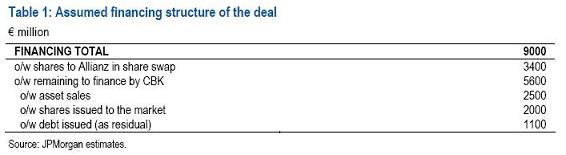

Today, the Financial Times blog site FT Alphaville revealed that JP Morgan Chase (JPM) had an interesting take on a Commerzbank offer, opining that the combined Commerzbank-Dresdner would be undercapitalised and need to go to market with a rights issue from the word go.

We believe that replenishing the capital base of a potential new group should be management’s primary concern and to this end we have added €2bln worth of capital measures which we think would ensure that core Tier 1 ratio of the assumed new entity would only fall to 5.7% (from Commerz stand-alone 6% at Q208). This €2bln could be raised either through a rights issue or through convertible issuance, for which CBK has already received approval by its EGMs (see Appendix II).

Note that our capital calculation includes an assumed €1.5bln benefit/capital gain deriving from the sale of some stakes, although we admit we have no exact details of their book value.

We would prefer capital of the new entity to remain close to 6%, which we calculate would require a further €1bln of capital issuance with a corresponding 4-5% negative impact on EPS. Note that for each €1bln of share capital issue, we estimate a 4-5% impact on EPS.

–FT Alphaville

JPM also offered a spreadsheet analysis to support their case:

{kind=link}

{kind=link}

Notice the highlight in table 11 shows the pro forma core Tier 1 capital ratio for Dresdner-Commerzbank in 2008 is under six percent. That won’t fly (click here to see why).

But, equally interesting is the signal from German labor union Ver.di that it would prefer a foreign buyer due to likely job losses from a Commerzbank-Dresdner deal, according to German magazine Spiegel. Below is an article translation:

The union Ver.di is basically open to a merger of Dresdner Bank with the China Development Bank (CDB). “We have always said that we have nothing against a foreign buyer. It always depends on what business model is behind it,” said a Ver.di spokesman on Wednesday. “Our concern is primarily about the preservation of jobs. Every concept which destroys jobs is a bad idea.”

In the case of a merger of Dresdner Bank with Commerzbank, with whom Dresdner parent group Allianz also negotiated, 20 to 25 percent of all jobs – in other words, from 10,000 to 12,000 bodies – would be at stake, in the view of Ver.di. In the case of a sale to a foreign company this would “very likely” not be the case. The Ver.di spokesman stressed that the union call for far-reaching employment guarantees by a sale of Dresdner Bank in any case.

–Spiegel Online

So, the game continues, with Commerzbank, the most likely buyer because of what we euphemistically call “synergies.” This is another way of saying job cuts. And, unfortunately, given Germany’s over-banked status, a reduction in staff makes sense, and not just financially.

What I find interesting here is that the Chinese Development Bank is a state-controlled organization. Just last week, the German ruling party CDU was looking to put the kibosh on Sovereign Wealth Funds (SWFs) taking over German companies (see story here). Then, it was not clear to me why. Now it makes a lot more sense.

With Western banks looking for capital any way they can get it and SWFs having that capital in spades, it seems like a match made in heaven. Let’s see what happens.